IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MARYLAND

(Southern Division)

BRUCE KONYA, et al.,

Plaintiffs,

v.

LOCKHEED MARTIN CORPORATION,

Defendant. |

No. 8:24-cv-00750-PJM |

DECLARATION OF THOMAS D. GOBER

GLOSSARY OF TERMS

Athene Entities | |

Apollo Global Management, Inc. | Apollo |

Athene Annuity and Life Company | Athene Iowa |

Athene Annuity Assurance Company of New York | Athene New York |

Athene Annuity Re Ltd. (Bermuda) | Athene Re |

Athene Holding Ltd. | Athene Holding |

Financial Terms | |

Captive Reinsurance | A form of self-insurance whereby, instead of diversifying its risk and liquidity by insuring part of its liabilities with a third-party insurer, the insurer creates a wholly-owned in-house subsidiary or affiliate to insure part of its liabilities. Captive reinsurance companies do not publicly file their financial statements as is required of all other U.S. insurers. |

Collateralized Loan Obligations (“CLOs”) | A single security backed by a pool of debt, often non- investment grade corporate loans. |

Private Equity (“PE”) Firm | A company that manages pooled investments of companies that are not publicly traded. |

Life Insurance and Annuity (“L&A”) Carrier | An insurance company that provides insurance coverage against disability or death, such as through an annuity that guarantees a stream of income for life or other defined period. |

Modified Co-Insurance (“ModCo”) | A type of reinsurance whereby the insurer (or ceding company) does not transfer the assets but reportedly transfers its regulatory capital requirements and asset risks to the reinsurer. Although the assets and liabilities are held at the ceding company, the reinsurer is responsible for those liabilities. |

National Association of Insurance Commissioners (“NAIC”) | A non-profit organization created and governed by the chief insurance regulators of all 50 states of the United States, the District of Columbia, and U.S. territories to set the standards for the U.S. insurance industry. |

Receivership | A process that occurs when an insurance carrier is unable to pay its liabilities. An independent entity takes control over the carrier’s assets to pay off its debts. |

Reinsurance | An issuer obtains insurance for its liabilities, which transfers its financial risks to another entity. |

Risk-Based Capital (“RBC”) Ratio | The measure is calculated by dividing an insurer’s total adjusted capital by its authorized control level as defined by the NAIC. It measures the amount of capital (or surplus) an insurer must hold to pay policyholders based on its level of risk. The higher the ratio, the safer the insurer. |

Surplus | An insurer’s total assets less its liabilities. |

Surplus-to-Liability Ratio | The measure is calculated by dividing an insurer’s liabilities by its surplus. It is used to gauge an insurer’s surplus adequacy (i.e., its ability to pay claims from policyholders). |

I, Thomas D. Gober, hereby declare as follows:

I. Qualifications and Professional Experience

- I am a Certified Fraud Examiner (“CFE”) whose primary career focus has been examinations and investigations of complex accounting fraud schemes in the insurance industry’s financial Except where otherwise stated, I have personal knowledge of the matters stated herein and if sworn as a witness could and would testify competently thereto.

- I am the President and owner of Thomas Gober Forensic Accounting Services located in Beaver, Pennsylvania. I have a Bachelor of Science from Belhaven College, Jackson, Mississippi and a Master of Business Administration from the Millsaps College Else School of Management, Jackson, Mississippi. I have had extensive experience, beginning in 1985, in conducting examinations of virtually all types of insurance I have spent over a decade assisting the United States Attorneys’ Office, the Federal Bureau of Investigation, and several other federal, state, and local law enforcement agencies in connection with criminal investigations of financial reporting within the insurance industry. In my service as a consultant, expert, and criminal investigator, I have reviewed and analyzed annual and quarterly financial statements, Statutory Reports of Examination, and all forms of documentation related to Financial Condition examinations.

- From May 1985 through February 1992, I was employed as an insurance examiner by the Mississippi Department of Insurance, where I obtained accreditation (Accredited Financial Examiner) and certification as a My duties involved financial statement analysis, insurance ratio calculations, statutory compliance, market conduct review, claims analysis time studies and preparation of examination reports. During my last three years with the Mississippi Department of Insurance, I served as Examiner- In-Charge. In my career as an insurance examiner, I conducted over 100 insurance company examinations, and it was my responsibility to examine the companies’ financial condition, integrity, and

transparency in accordance with the National Association of Insurance Commissioners (“NAIC”) Examiners Handbook Guidelines and all applicable state laws and regulations.

- I have provided expert testimony in civil and criminal actions in federal, state, and local courts located in Alabama, California, Colorado, Mississippi, New York, Pennsylvania, Virginia, Washington state, and the District of Columbia in my role as a CFE. Subsequent to my tenure with the Mississippi Department of Insurance, I have provided expert services for both plaintiffs and defendants in civil and criminal matters. I have 39 years of education and experience in statutory accounting of insurance companies, enhanced through my deep experience regarding insurance company financial reporting. The bulk of my work as a CFE is related to complex accounting issues in the insurance and reinsurance industries.

- I have also spent the past five years evaluating risk characteristics of life and annuity

issuers.

II. Athene Annuity and Life Company and the Profound Risks Associated with Lockheed Martin Corporation’s Pension Risk Transfer

- I have examined publicly available records of the financial condition of Athene Annuity and Life Company (“Athene Iowa”), a life insurance and annuity (“L&A”) carrier domiciled in Iowa and the issuer of the Group Annuity Contracts at issue in this case for the Lockheed Martin Corporation Salaried Employee Retirement Program and the Lockheed Martin Aerospace Hourly Pension Plan. Lockheed Martin Corporation is referred to as “Lockheed.” I understand that Athene Annuity Assurance Company of New York (“Athene New York”) is the issuer for Lockheed retirees who reside in New For purposes of my declaration, the observations related to Athene Iowa also apply to this issuer.

- I have also evaluated various other Athene Iowa affiliates, including Athene Annuity & Life Assurance Company, Venerable Insurance and Annuity Company, and Corporate Solutions Life Reinsurance Company, among Based on a variety of factors, including its structure, its assets, and

the higher premium that the market requires for its bonds because of their higher risk, Athene Iowa is one of the riskiest annuity providers in the Pension Risk Transfer (“PRT”) space for reasons set forth below. These reasons are not an exhaustive list as there are other factors that contribute to the higher risk associated with Athene Iowa. These risks are well documented by numerous industry publications which have been written regarding Athene Iowa’s structure and risk, and stand in contrast to traditional life insurers.1 These publications are readily available to any fiduciary or investment professional who conducts an analysis of the risk associated with Athene Iowa’s annuities.

- As described in further detail below, rather than diversifying its risk by using a third-party, secure reinsurer, Athene Iowa transfers its risk to in-house affiliated reinsurers, such that the reinsurer provides no independent capital or expertise. Moreover, Athene Iowa has based this in-house reinsurer in Bermuda, where regulatory standards are lax compared to U.S. standards and fewer reserves are

- Athene Iowa is under the ultimate control of “Marc Rowan, Joshua Harris and Leon Black” through Apollo Global Management, Inc. (“Apollo”), a “private equity firm specializing in investments in credit, private equity and real estate ”2 In recent years, numerous federal agencies and the NAIC have expressed concerns that private equity (“PE”) controlled L&A carriers no longer resemble traditional life insurers, taking greater investment risks relative to surplus, forming reinsurers in house rather than diversifying risk by using third party reinsurers, headquartering their operations offshore where there is lower regulatory protection, loading up their balance sheet with investments held

1 Eichorn, David, Pension Risk Transfers (PRT) May Be Transferring Risk to Beneficiaries, NISA, 2022, https://www.nisa.com/perspectives/pension-risk-transfers-prt-may-be-transferring-risk-to-beneficiaries/; Indap, Sujeet, How financial engineering in Bermuda boosted Apollo, Financial Times, Aug. 6, 2023, https://www.ft.com/content/09f2d8af- 08ec-456a-9692-c5a11ebffd8d; Morgenson, Gretchen, As insurance companies take over pension plans, are your payments at risk? NBC News, June 14, 2020, https://www.nbcnews.com/business/personal-finance/insurance-companies-take-over- pension-plans-are-your-payments-risk-n1229226; Williams Walsh, Mary, Risky Moves in the Game of Life Insurance, The New York Times, Apr. 11, 2015, https://www.nytimes.com/2015/04/12/business/dealbook/insurers-bypass-rules-to-add- hidden-risk.html.

2 S&P Global, https://www.capitaliq.spglobal.com/web/client#company/profile?id=4204256.

by the private equity parent and related parties, and concealing those risks through opaque transactions with affiliated reinsurers.

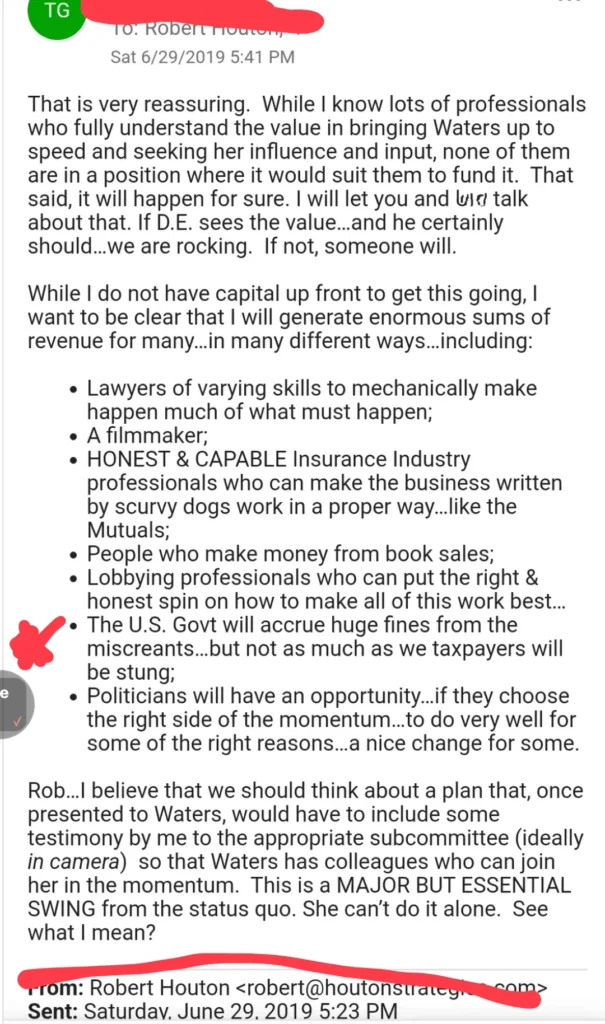

- Below is a snapshot of Athene Iowa’s statutory total assets, total liabilities, and surplus as of December 31, 2023. Athene Iowa’s surplus to liabilities ratio is 44%, while the U.S. L&A carriers’ national average is over 400% higher at 7.49%.3

- This is important. Surplus is a simple measure: total assets less total liabilities. It is the only buffer between an insurer’s solvency or The surplus-to-liability ratio gauges an insurer’s surplus adequacy (i.e., its ability to pay claims from policyholders). When an insurer’s assets are devalued, or its liabilities are increased, those adjustments are deducted (or reduce) the amount of surplus. The risk of such adjustments to surplus is greater when an insurer holds riskier assets.

- Other L&A carriers that are of a similar size to Athene Iowa have a much more significant surplus when compared to liabilities. When Athene Iowa touts its ample surplus, it is referring to the combined surplus of its holding company (Athene Holding ) (“Athene Holding”). But an analysis of Athene Iowa’s statutory annual statement for December 31, 2023, reflects one of the thinnest surplus levels, as set forth above, relative to its size and risk appetite, among all U.S. L&A carriers.

- The graph below reflects surplus-to-liability ratios of several traditional insurers compared to Athene Iowa. The lowest of these has almost four times the ratio of surplus to liabilities as does Athene New York Life’s surplus-to-liability ratio is more than eight times that of Athene Iowa.

3 The national average of U.S. L&A carriers was determined by totaling the liabilities and surplus for 688 insurers from their statutory annual statements, and then dividing the total surplus by the total liabilities.

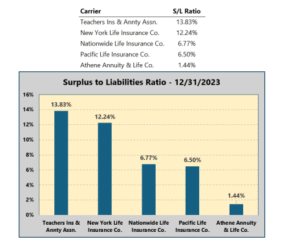

- Seen another way, surplus levels of four carriers of substantially similar size are compared below.

- While a surplus-to-liabilities comparison between Athene Iowa and other safer annuity providers is stark, more significant is the comparison of concentrations of risk taken in their investment portfolio and the lack of transparency in their reinsurance ceded to captive affiliates, as opposed to diversifying risk with third-party reinsurers. Reinsurance refers to an issuer obtaining insurance for its liabilities, or in other words, transferring its financial risks to another entity.

- For example, as a pure mutual insurance company, New York Life Insurance Company (“New York Life”) has a substantially more traditional, lower-risk investment portfolio than Athene Iowa, and New York Life has no captive and non-transparent reinsurance. Pacific Life Insurance Company (“Pacific Life”), as part of a mutual holding company group, also has a much more traditional and safer investment portfolio than Athene. While Pacific Life has a nominal amount of captive affiliated reinsurance, only a small fraction of its surplus is impacted, and it is not On the other hand, the amount of Athene’s non-transparent, captive-affiliated reinsurance is more than 5,000% greater than that of its surplus.

- Arm’s-length reinsurance with a third-party reinsurer can provide substantial benefits to policyholders since it increases liquidity and diversifies risk. On the other hand, offloading risk to a wholly-owned reinsurance affiliate within the same group of companies under common control is not arm’s length and does not represent bona fide risk transfer.

- The lack of transparency surrounding Athene Iowa’s reinsurance “ceded to” (or placed with) a captive or non-transparent affiliate is shocking. As of December 31, 2023, Athene Iowa’s reinsurance included more than $15 billion ceded to affiliates. In addition to those reinsurance placements, Athene Iowa engages in substantial amounts of Modified Co-Insurance (“ModCo”) with its offshore affiliate, Athene Annuity Re Ltd. (Bermuda) (“Athene Re”).

- In layman’s terms, ModCo is a type of In a ModCo transaction, Athene Iowa

maintains control over its assets and liabilities while transferring its regulatory capital requirements

associated with the asset risks (i.e., sufficient capital to pay claims) to its offshore affiliate Athene Re. While ModCo enables the ceding carrier (i.e., Athene Iowa) to hold all assets involved in the transaction, the U.S. carriers purport to transfer the “asset risks” associated with those assets to their offshore affiliate (i.e., Athene Re). However, the liabilities and asset risks remain shared by Athene Iowa and Athene Re in accordance with the relevant ModCo agreements. Based on the reported transfer of asset risks, the U.S. carrier excludes those asset risks from its crucial Risk-Based Capital (“RBC”) ratio, resulting in much lower required minimum surplus.

- The RBC ratio considers how risky the insurer is and measures the amount of capital (or surplus) an insurer must hold to pay policyholders based on its level of If an insurer fails to meet the minimum RBC ratio, it must provide further capital to ensure adequate solvency to protect against the potential loss of default or be placed in receivership. The detection of the need for higher surplus is prevented if certain risky assets are excluded from the formula.

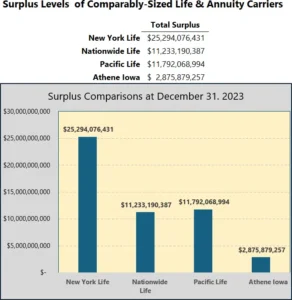

- As of December 31, 2023, Athene Iowa reported in its statutory annual statement ModCo (funds withheld) transactions totaling $141.5 billion. In recent years, there has been much written about ModCo obfuscation. As reported, ModCo is being increasingly used by certain U.S. carriers in transactions with their offshore affiliates, as in this specific matter, to substantially reduce the U.S. carrier’s minimum required surplus to meet claims from 4 Athene Iowa, through the use of $141.5 billion of ModCo with its offshore affiliate, is able to report a much lower surplus level. It is apparent that the ceding company (here, Athene Iowa) is maintaining substantially less surplus than it needs to protect pensioners.

- The graphic below compares Athene Iowa’s use of ModCo ceded to offshore affiliates with four of its peers as of December 31, 2023.

4 Kyeonghee Kim, et al., Regulatory Capital and Asset Risk Transfer, Journal of Risk and Insurance, June 22, 2023, http://doi.org/10.1111/jori.12441; Warren S. Hersch, Critics Call for Reinsurance Crackdown After Paper Exposes Flaws, Life Annuity Specialist, Oct. 21, 2022, https://www.lifeannuityspecialist.com/pc/3794974/490354?all=true.

- All transactions with captives or offshore affiliates lack transparency because the assuming affiliate (e., Athene Re) is domiciled in a jurisdiction where the reinsurer does not report under

U.S. Statutory Accounting Principles (“SAP”). In fact, despite Athene Iowa’s Bermuda affiliates’ substantial interdependence, U.S. insurance examiners do not conduct examinations of them, as is recommended by the NAIC under the coordinated examination process.

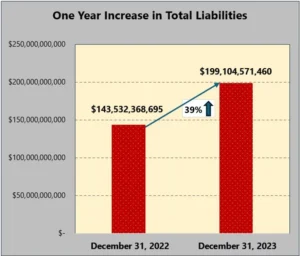

- A comparison of Athene Iowa’s most recent statutory annual statement dated December 31, 2023, with its statutory annual statement from the prior year, reveals a continuing pattern of rapid growth of liabilities and yet, surplus that fails to keep up with its increased size and risk This data is shown in the following charts.

- Note above that in just one year, total liabilities increased by $55.6 billion to nearly $200 billion while surplus increased to $2.9 billion, again leaving a thin surplus to liabilities ratio of 44% compared to the national average which is greater than 7%. Thus, the average insurer’s relative surplus is more than 400% higher than Athene Iowa’s surplus. Athene Iowa’s outsized concentrations of higher-risk asset categories and significant affiliated and non-transparent offshore reinsurance relative to such a thin level of surplus indicates that the protection of policyholders is not placed as a high priority relative to the actions of traditional insurers. Indeed, Athene Holding and Apollo, when speaking to investors, regularly tout their control and use of Athene Iowa’s “sticky capital.” This is in reference to

their access to policyholder funds. These assets are “sticky” because they are tied to long-term annuity contracts, and thus, less likely to be withdrawn by policyholders.

- Athene Iowa has significant concentrations of higher risk, less liquid, and complex investments in amounts that dwarf its surplus. If even a fraction of the high-risk assets, including commercial mortgages, commercial mortgage-backed securities, affiliated party structured credit instruments, and “Other Loan-Backed” bonds, for instance, turned out to be problematic, Athene Iowa’s surplus would be written down below zero and would require regulatory intervention.

- Even though pensioners have no say in the choice of an annuity provider, funds transferred out of a pension plan and handed over to Athene Iowa in connection with PRT transactions can never be withdrawn by pensioners. There are no cost of living adjustments, as all payment obligations are fixed and determined at contract A retiree with a lower risk appetite whose pension was transferred to Athene Iowa does not have the option to move her pension to a safer, less risky alternative.

- Many reputable commentators have recently raised alarms regarding increasingly risky practices undertaken by PE-controlled insurers, including through the use of Collateralized Loan Obligations (“CLOs”), ModCo, and private credit, as well as the opaque nature of non-public private equity investments, which underlie the assets of these PE-backed insurers.5 Athene Iowa’s holding company structure increases risk borne by policyholders. In a filing with the SEC, Exhibit 21.1,6dated February 25, 2022, Apollo Global Management disclosed its “List of Subsidiaries” that total 1,114 entities, including:

- 383 in the Cayman Islands,

- 32 in Anguilla,

- 30 in Luxembourg,

5 Appelbaum, Eileen. Beware of Private Equity Gobbling Up Life Insurance and Annuity Companies, Center for Economic Policy Research, January 2022; Brown, Sherrod, Letter to the Federal Insurance Office and National Association of Insurance Commissioners re: private equity s involvement in life insurance, Mar. 16, 2022; Fabio Cortes et al., Global Financial Stability Report: The Last Mile: Financial Vulnerabilities and Risks, Chapter 2, Apr. 2024, at 70–71.

6 Athene Holding, Ltd., Exhibit 21.1: List of Subsidiaries, https://www.sec.gov/Archives/edgar/data/1411494/000141149422000014/exhibit211q42021.htm.

- 4 in Mauritius, and

- 12 in the Marshall

- This means that more than one-third of Athene Iowa’s “affiliates” are offshore and not subject to SAP. The global structure of Athene Iowa’s holding company’s system across multiple jurisdictions, which do not report under SAP, exposes Athene Iowa policyholders to greater risk due to less transparency and substantially less conservative accounting standards.

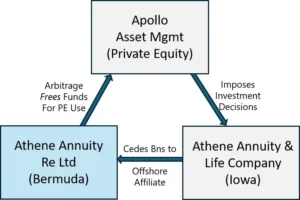

- Athene Iowa reinsures nearly all of its liabilities through its Bermuda-based, wholly- owned reinsurer, Athene Re. This makes it unlikely for Athene Iowa to be identified as posing risk to financial stability in the S. because of the lack of transparency regarding the quality or amount of assets securing the pension obligations of retirees and their beneficiaries. The diagram below shows how this structure, referred to in the industry as the Bermuda triangle, works.

- The Bermuda triangle arrangement results in Athene Iowa investing in companies owned by Apollo and providing large asset management fees to Apollo, all while adding significant risks for retirees. The billions (“Bns”) ceded from Athene Iowa to Athene Re, and ultimately to Apollo for management, are shown. Should Athene Iowa face a liquidity crisis or shortfall, Athene Iowa is almost entirely dependent on IOUs from Athene Re. Thus, Athene Iowa is dramatically under-reserved relative to its peers. SAP were designed to protect U.S. consumers—to make sure the carrier is not only solvent today but will be solvent and able to fulfill the long-term promises made to all of their policyholders.

- The fact that Bermuda entities report under Generally Accepted Accounting Principles (“GAAP”) and S. based insurers report under the safer SAP makes it even more difficult to see the full risk of Athene’s financial condition. The statutory annual statement required by SAP is far more complex and detailed than the GAAP Form 10-K. However, once U.S. policyholder liabilities are shifted offshore, many of those essential details disappear.

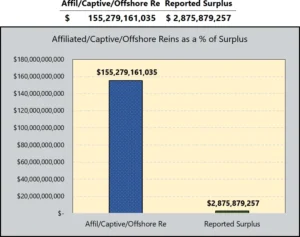

- By Apollo causing most of the business to be sent to offshore affiliates that do not file under SAP, it makes opaque the solvency or liquidity of the offshore reinsurers. Relevant here, as of December 31, 2023, Athene Iowa is counting on more than $155 billion of reinsurance with its own captives and offshore affiliates. See supra ¶ 24. Comparing that amount in affiliated reinsurance with Athene Iowa’s total reported surplus (its only buffer between a viable carrier and one in receivership) of

$2.88 billion, the gravity of the lack of transparency and risk of the offshore reinsurers is of great concern. The fact that the Bermuda-based Athene Re controls such a large percentage of Athene Iowa’s assets would make an orderly liquidation under state insurance laws unwieldy and costly as marshalling assets located in Bermuda for the benefit of pensioners will not be a simple and straightforward process.

- The risk of a collapse of an annuity provider is present here with Athene Iowa. In 1991, the Executive Life Insurance Company (“ELIC”) was placed into conservation by then-Commissioner of Insurance of the State of California, John Garamendi, due to an enormous concentration in high-risk, high-yield bonds that were procured through Drexel Burnham Lambert (“Drexel”). Shortly thereafter, the Superintendent of Insurance of the State of New York took control of the Executive Life Insurance Company of New York (“ELNY”) due to the adverse publicity surrounding ELIC’s takeover by the California Insurance Department, and to prevent a hazardous number of surrenders of ELNY annuity

- The collapse of Drexel led to ELIC defaulting on its annuity contracts, impacting tens of

thousands of pensioners. ELIC and ELNY’s parent company, First Executive Corporation, filed for

bankruptcy in April of 1991. ELIC’s junk bond portfolio was subsequently acquired at a fire sale price by none other than Leon Black, who used the bond portfolio to create Athene’s parent company, Apollo.

- ELNY remained in rehabilitation from 1991 until it was declared insolvent in 2012. The ELNY liquidation was finalized in August 2013 with the creation of the Guaranty Association Benefits Company (“GABC”), a Washington, D.C.-based captive insurance company. GABC continues to make reduced payments to ELNY annuitants, many of whom saw losses of more than 50% of their allegedly “guaranteed” annuity payments.7 According to the ELNY Restructuring Agreement, GABC is expected to make reduced payments until the last ELNY annuitant dies – which may not occur for another 50

- The similarities between the Executive Life Insurance companies and the Athene companies are remarkable and frightening.

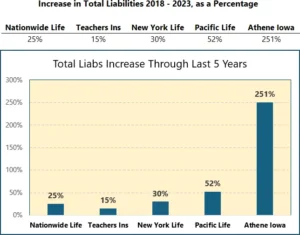

- Athene Iowa’s liabilities have surged at alarming rates in recent years, which has further contributed to the risk borne by policyholders and pensioners. The chart below identifies the increase in liabilities as a percentage of assets for Athene and four other insurance carriers from 2018 through 2023.

7 See Agreement of Restructuring in Connection with the Liquidation of Executive Life Insurance Company of New York, Apr. 23, 2023, and Schedule 1.15 (List of Contracts).

- Even a cursory review of Athene Iowa’s capital and surplus should have raised red flags for any plan fiduciary or investment professional, and the extent to which Athene Iowa depends on reinsurance with an affiliate that does not report under SAP should have ended the inquiry altogether.

- The bond ratings of the issuer can be used to examine the creditworthiness of the annuity provider because the factors that influence bond pricing are applicable to an annuity. A bond is a comparable investment to an annuity because the issuer of both types of investments promises to provide a future stream of income to the holder. The bond market provides a reliable indicator of the credit risk of an issuer through a bond’s credit The spread is the difference between a bond’s yield compared to the risk-free U.S. Treasury bond of the same maturity. It measures the credit risk of the insurer by placing a premium (or higher yield) on the bond to compensate the holder for assuming the additional risk of the lower-quality issuer. By comparing the credit spread among alternative annuity providers, a plan fiduciary or investment professional can observe the market’s assessment of their relative credit risk. In the case of Athene (using bonds issued by Athene Global Funding), the credit spread on those bonds is up to 14% higher—or riskier—than traditional annuity providers, such as New York Life.8

- The differences in bond credit ratings are also material as they indicate the likelihood of default among Athene Iowa has a Moody’s rating of A1 (or A+ for S&P) in contrast to New York Life that maintains a credit rating of Aaa (or AAA for S&P). Moody’s reported the average cumulative issuer-weighted default rates by issuer credit rating from 1970 through 2021. Over the 20-year time horizon, the default rates for riskier issuers are apparent. The default rates are only 0.7% for Moody’s Aaa ratings compared to the default rate of 5.0% for its A ratings. This means that over a 20-year time horizon, the approximate default rate of Athene Iowa’s bonds is almost seven times riskier than those of

8 Eichorn, David, Pension Risk Transfers (PRT) May Be Transferring Risk to Beneficiaries, NISA, 2022, Figure 2 and Appendix B.

a high-credit quality issuer. This differential is yet another indicator of the risk that pensioners have assumed with Athene Iowa. Many annuitants will live decades into the future and bear these risks.

- Accordingly, rather than relying solely on the credit ratings of Athene Iowa, a plan fiduciary or investment professional can also rely on the market to measure creditworthiness of an annuity provider. Since there is a market for annuities, the market will set a value for how much the same cash flows are worth, when paid by different issuers, on the basis of how much more or less the market charges those companies to borrow money via issuance of If an annuitant receives the same cash flow, but from an issuer of lower creditworthiness, it is a loss for the annuitant. Accordingly, the market will assign a lower price for an annuity issued by a riskier annuity provider to cover a similar stream of future payments to the annuitant.

- Based on the actual market, the Lockheed retirees’ Athene-issued annuities are worth measurably less than they would be worth if issued by a traditional insurer such as MassMutual Insurance Company (“MassMutual”) or New York Life, for example. The latter are insurers of high credit quality, which means to the annuitant that there is a greater chance that they will receive all of the payments to which they are entitled. If the annuity were purchased on the open market, any rational annuitant, if offered an identical annuity at the same price from these three issuers, would choose the one from MassMutual or New York Life, rather than the one from Athene Iowa (or Athene New York)—or, equivalently, would insist on paying a lower price for the annuity bought from these insurers because of its lesser value.

- The amount of this loss of value of the pensions of the Lockheed retirees whose pensions have been transferred to Athene Iowa (or Athene New York) is real and substantial in dollar terms.

- In sum, Apollo, Athene Iowa and Athene Re have chosen to create their organizational

structure in a manner that exposes each of their affiliates to a heightened risk of failure due to the failure of another affiliate (domino effect). They have created their high levels of interdependence through

investments in each other, management and service fees to each other, guarantees of each other, and reinsurance with each other.

- By simply reviewing publicly available statutory financial statements, any reasonable independent fiduciary would be able to see just how dependent Athene Iowa is on Athene Re and just how much exposure Athene Iowa has to risky assets, non-arm’s length affiliated party transactions, and highly suspect and opaque ModCo.

I declare under penalty of perjury that the foregoing is true and correct to the best of my knowledge and belief.

Executed this 28th day of May, 2024, in Beaver, Pennsylvania.